As one of the Gartenberg tenants, mutual fund directors are charged with assessing how the adviser shares economies of scale with fund investors. In recent years, a long run of market performance likely boosted firms’ and funds’ assets under management (depending, of course, on the strategies in which the funds were invested). Depending on the impact of fund demand and net flows, there are good odds that the economies of scale discussions at the annual contract renewal meetings covered AUM growth and correlating impacts to investments, operations, and fund expenses.

As market conditions changed dramatically in 2022, however, the contract renewal discussion may now pivot (or maybe already has) to a focus on sharing economies of scale in the context of a loss in AUM. Directors now may be responsible for overseeing increasing expenses, which can become a more complex, and possibly less pleasant, boardroom discussion.

The first thing to look at is a fund’s fee structure, as this will help in determining whether a fee increase might be appropriate. In times of AUM growth, it is the responsibility of directors to ensure fixed and/or semi-variable non-advisory expenses are tracking AUM growth. Assessing those expenses in the same manner when AUM is shrinking is equally important. When fees are spread across fewer assets, the basis point fee logically will increase in line with the fund size.

Breakpoints

Another consideration is the advisory fee and any breakpoints that might be included as part of the fee schedule as a tool to share scale. As AUM declines, the funds may no longer meet their set breakpoints and therefore the effective advisory fee will go up.

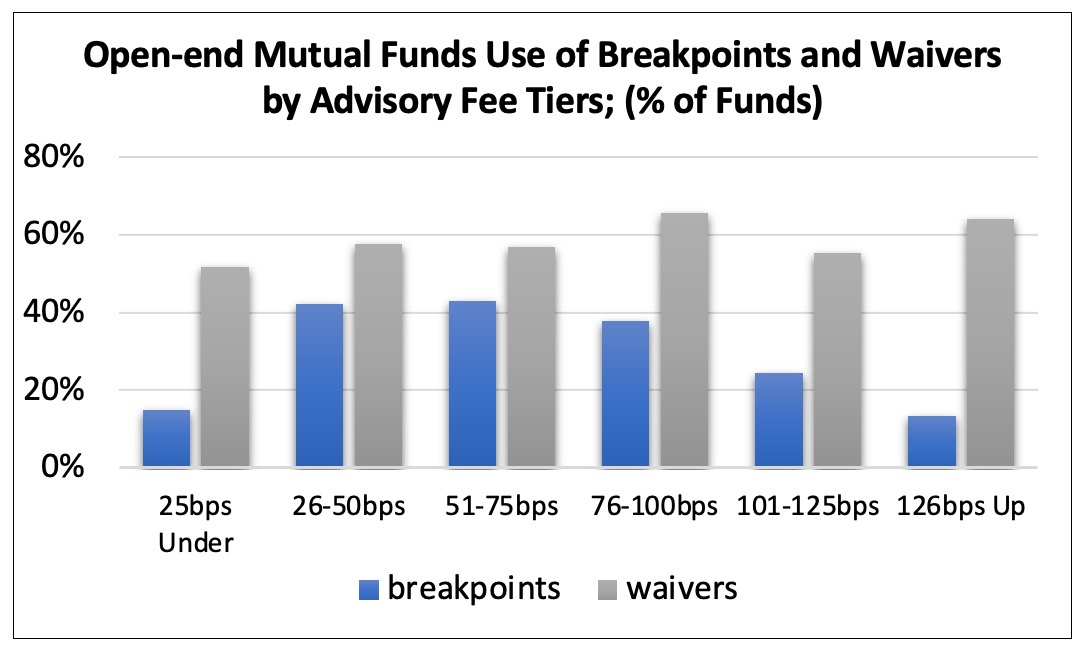

This is a concern and will impact some funds after the market performance of 2022, but the industrywide effect is likely to be less than anticipated. This is because for all U.S. open-end mutual funds, only about a third have breakpoints in their fee schedule, and at the end of 2022, only 16% of those with breakpoints were meeting the first tier in the breakpoints schedule (see chart). The use of breakpoints in ETFs is far lower.

For those funds that do have breakpoints in place, the directors will be charged with assessing if they are comfortable with any increase in advisory fees resulting from declining AUM. There may be some important considerations to discuss in the process to ensure any individual fund fee changes aren’t implemented simply in reaction to what have proven to be volatile markets. Rather, directors may want to revisit the original discussions around the fee schedule implementation and address the following questions in the context of current circumstances:

- What was the initial logic in structuring the advisory fee schedule, and is it still applicable? Did the breakpoints adequately share scale during growth and now return to fee levels at previous AUM?

- Were the breakpoints established at AUM tiers that weren’t initially reasonable to sustain or grow?

- Discuss with the adviser what the anticipated future AUM might be. Is it reasonable that AUM may fluctuate in the short term but return to existing breakpoint levels in the long term?

- Were the breakpoints created with similar fee structures for all funds in the family to have a similar pricing strategy?

- Were the breakpoints created at a trust or firm level, and what is the resulting revenue and profitability impact of changing them?

Directors should remember that they can approve lowering the asset tiers in the breakpoint fee schedule or inserting additional tiers as long as there is no decline in the level of services. However, the breakpoint levels cannot be reinstated (or removed) without shareholder approval, which can be a long and costly effort.

Waivers

The use of voluntary waivers is another approach that may be considered when attempting to control fees. And in fact, the use of waivers has become more common than the use of breakpoints; waivers at all advisory fee levels are more prevalent than breakpoints (see chart). Of course, waivers can be in place for reasons beyond reducing fees for competitive purposes, including to cap expenses on small funds or reimburse underlying fund holdings. More recently, waivers have also been used in relation to yield for money market funds.

Because there are different reasons to use voluntary fee waivers, they are used more consistently across funds with varying advisory fee levels. Breakpoints, on the other hand, are used less at both ends of the fee spectrum. For example, very low-fee funds—often money market and fixed-income funds—understandably aren’t as likely to implement breakpoints, while comparatively high-fee funds often are specialty funds with smaller AUM levels. As the most common first breakpoint level is $500 million in AUM, many funds have not reached—and may not ever reach—that scale. This is when expense caps and waivers become a more effective tool to control expenses.

If directors become concerned about increasing or uncompetitive fees with fluctuating AUM, reducing fees through a waiver (rather than a contractual change) allows expenses to be controlled for a period of time without requiring shareholder approval to reverse course when market conditions improve. This is an advantage of waivers over breakpoints, but as with any change to the advisory fee, the impact on the revenue and profitability of the fund and the firm should be thoroughly analyzed before implementation. This calls for a thoughtful approach to how any changes would align with the pricing strategy of other firm funds and products.

Comfort Level

With loss of AUM, there are additional considerations for directors in their role as overseers that go beyond fees and which impact the adviser and, ultimately, the investors themselves. For instance, when AUM grow, the adviser often shares that scale by reinvesting in the business, including allocating budget to marketing, technology, staffing, and/or infrastructure. With lower AUM and less revenue, directors may consider inquiring if these efforts are ongoing and if so, to what extent. Such discussions, which should cover not just the fund-by-fund advisory contract profitability but also the total firm-level profitability, enable the directors to achieve a level of comfort around overall financial viability and the adviser’s ability to provide promised investment, legal, compliance, and operations services to investors.

Oversight of fees is an important part of a director’s job and balancing that task within the context of profitability—at both the fund level and firm level—while also addressing the other Gartenberg considerations, is part of the process. Considering and discussing the appropriate changes in fees, as AUM both increases and declines, should lead to a best-case scenario for investors and peace of mind for the directors.

Sara Yerkey is a partner at Management Practice Inc., where she focuses on mutual fund governance, contract renewal, and profitability analysis. Before joining MPI in 2006, she worked for five years in the corporate finance division at Janus Capital Group and before that in the financial analysis and product sector at Standard & Poor's.